The tax break looks great, but what could go wrong?

Open enrollment often puts one number in bright lights: the tax break. An HSA can cut taxable income, grow without current tax, and pay medical bills with tax-free withdrawals. On paper, that can make an HDHP look like the smart choice fast.

What gets missed is how the money leaves your account during a real year. If you need imaging in February, a few specialist visits in spring, or outpatient surgery before you have built the HSA balance, the deductible is not theoretical. You may need to cover thousands from cash while still paying regular bills. That is where a plan that looked cheaper on a spreadsheet can start to feel expensive, and why the cash question comes first.

Can you cover a bad medical month from cash?

A bad month usually does not arrive as one giant bill. It shows up as an ER visit, a scan, lab work, and a follow-up appointment that all land before your HSA has had time to build. If your plan has a $3,500 deductible and it is March, the question is not whether the HDHP can win over a full year. It is whether you can pay that amount now without carrying a credit-card balance or skipping something else important.

This is where cash flow matters more than tax math. A household with $15,000 in accessible savings can absorb an ugly month very differently from one that is saving steadily but keeps most money tied up in retirement accounts or home equity. Even a solid income does not fix timing. Bills often come due before reimbursements, payroll contributions, or provider corrections settle.

If covering the deductible would force borrowing, the cheaper premium can stop being the cheaper option. That is the point where predictable care starts to change the bet.

If care is predictable, the gamble changes

That shift becomes easier to see when you already know some care is coming. If you take expensive prescriptions every month, see a specialist on a set schedule, or have a child in therapy, your spending is not a surprise. In that case, the HDHP is less of a clean tax play and more of a timing problem: how much you pay early, how fast you hit the deductible, and what each visit costs before the plan starts sharing more of the bill.

A PPO or EPO can look worse on premiums and still cost less over the year for this kind of household. Copays for office visits, better drug coverage, or a lower deductible can beat the HSA advantage once the services are steady and repeat. The hard part is that “predictable” is rarely perfect. A condition can stay stable for six months, then require imaging, a procedure, or a brand-name drug switch. That is why the next step is to test the numbers across more than one kind of year.

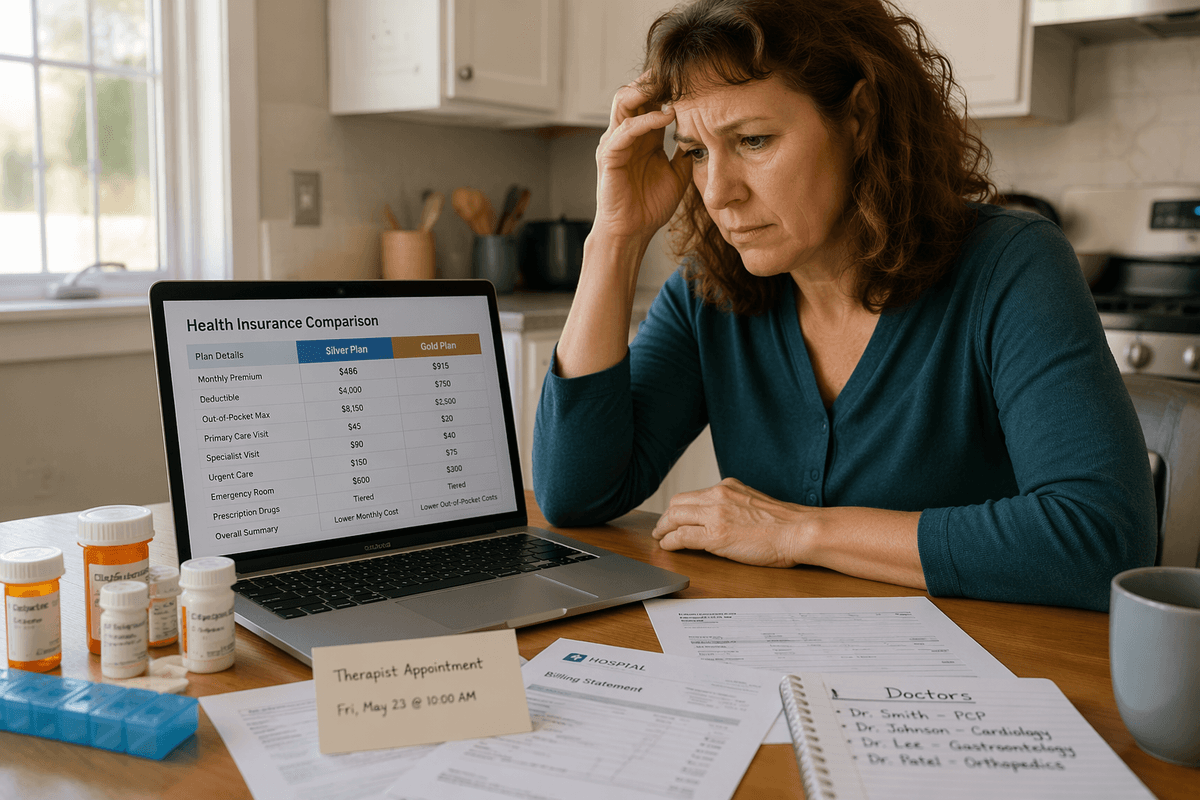

What do your low, medium, and bad-year numbers show?

The clearest comparison usually comes from three quick scenarios, not one confident guess. Start with a low-use year: annual physical, a couple of sick visits, maybe one generic prescription. Then run a medium year with several specialist appointments, routine labs, and one imaging bill. Then test a bad year: ER visit, outpatient procedure, higher drug spending, or a few months of recurring care. Put real numbers beside each plan: premium, employer HSA contribution, deductible exposure, coinsurance, and what you would actually pay out of pocket.

This often changes the picture fast. An HDHP may still win in the low year, especially if the employer adds meaningful HSA money. In the medium year, that lead can shrink or disappear once you price visits before the deductible and include prescription costs. In the bad year, the result often depends less on tax savings and more on how close you get to the out-of-pocket maximum.

Do not force precision that you do not have. The point is to see the range. If one plan only works when almost nothing happens, while the other stays manageable across all three cases, that is a strong signal. Then one number deserves more respect than the rest.

Your doctors may matter more than the premium gap

A common surprise shows up when you check whether your regular doctors, hospital, therapist, or drug list fit the cheaper plan. If a specialist is out of network, or a hospital system is missing, the premium difference can stop mattering fast. One surgery with the wrong facility, or months of seeing a therapist at out-of-network rates, can wipe out what looked like savings.

This matters most when care is already in motion. If you are managing a chronic condition, ongoing therapy, or a child’s specialist care, switching plans can mean switching doctors, starting prior authorizations again, or paying more until referrals and records catch up. Even when the HDHP uses the same broad network on paper, the drug formulary and visit pricing can still change what you pay.

So check the actual names: doctors, clinics, hospitals, and prescriptions. A plan is not cheaper if it pushes you toward providers you do not want to use or bills you like you chose the wrong year to get sick. That is why the number with the most bite is usually not the deductible by itself.

The out-of-pocket max is the number to respect

That shows up most clearly when a year goes sideways. A deductible feels like the hurdle because you hit it first, but the out-of-pocket maximum is the cap that tells you how much damage the plan can do in a bad year. If one option has a $4,500 max and another has an $8,700 max, that gap matters more than a modest premium difference once care gets heavy.

Use it as a stress-test number, not a background detail. Ask a plain question: if the worst covered year happened, could you absorb that amount without debt, raiding retirement accounts, or putting routine expenses on a card? The catch is that this number still does not cover everything. Out-of-network bills, non-covered drugs, balance billing where allowed, and family deductibles can leave you paying more than you expected.

Respect the ceiling, then work backward. The right plan is usually the one whose bad year you can survive without your finances becoming the second problem.

Choose the plan you can live with all year

That usually means picking the plan that stays workable in an ordinary month and does not become a financial mess in a bad one. If the HDHP only looks best when nothing happens, when every doctor stays in network, and when you can fund the HSA quickly, you do not really have a margin for error. Real years rarely cooperate that neatly.

A useful rule is simple: favor the option that you can pay for without stress, not the one that wins only under ideal assumptions. Tax savings matter. So do lower premiums. But a plan you can carry through job changes, surprise bills, and uneven cash flow is often the better decision.